Blog Categories:

Your Tax Prep Checklist: 10 Things to Do Before the IRS Comes Knocking

Being your own boss sounds glamorous. You control your time, build your vision, and keep the profits. But behind the freedom lies a reality that often surprises new entrepreneurs. The truth is, there are hidden costs that can quietly eat away at your bottom line. The good news is you can spot these traps early and take steps to reduce them. Let’s look at the most common hidden costs of entrepreneurship and how to slash them before they derail your success.

Taxes are never fun, but for small business owners, being unprepared can turn them into a nightmare. Late filings, missing receipts, and disorganized books all make the IRS more interested in your business than you want them to be. That is why having a clear plan matters. Here is a practical small business tax preparation checklist to help you stay audit ready and stress free.

🔴 1️⃣ Gather All Income Records

The IRS wants to see every dollar that came into your business. Forgetting even small amounts can create big problems.

Checklist Table: Income Records

🟢 2️⃣ Collect Expense Documentation

Your deductions only count if you have proof. Keep receipts and digital copies organized.

Checklist Table: Expense Categories

🔵 3️⃣ Reconcile Bank and Credit Card Accounts

Make sure your bank statements match your bookkeeping. If they do not align, the IRS will ask why.

Checklist Table: Reconciliation Steps

🟣 4️⃣ Organize Payroll Records

If you pay employees or contractors, keep payroll reports, W2s, and 1099s in order.

Checklist Table: Payroll Records

🟡 5️⃣ Review Quarterly Estimated Tax Payments

Small businesses are expected to pay estimated taxes. Missing these can lead to penalties.

Checklist Table: Estimated Payments

🟠 6️⃣ Track Business Mileage

Mileage is one of the most commonly missed deductions. You need a clear log.

Checklist Table: Mileage Tracking

🔴 7️⃣ Review Asset Purchases and Depreciation

Large purchases like equipment or vehicles can be written off or depreciated.

Checklist Table: Asset Review

🟢 8️⃣ Double Check Tax Credits

Credits can save you thousands, but many small business owners miss them.

Checklist Table: Common Tax Credits

🔵 9️⃣ Prepare Your Financial Statements

Your P&L, balance sheet, and cash flow statement are the backbone of tax prep.

Checklist Table: Financial Reports

🟣 🔟 Schedule a Final Review with Your Accountant

Even if you prepare everything yourself, a professional review can save you from costly mistakes.

Checklist Table: Accountant Review Items

The Bottom Line

Tax season does not have to be a headache. By following this small business tax preparation checklist, you will reduce stress, avoid penalties, and be ready if the IRS ever comes knocking.

👉 Subscribe to Tea on the Ledger for more practical strategies and financial tips that help you stay audit proof and confident year round.

The Hidden Costs of Being Your Own Boss (And How to Slash Them)

Being your own boss sounds glamorous. You control your time, build your vision, and keep the profits. But behind the freedom lies a reality that often surprises new entrepreneurs. The truth is, there are hidden costs that can quietly eat away at your bottom line. The good news is you can spot these traps early and take steps to reduce them. Let’s look at the most common hidden costs of entrepreneurship and how to slash them before they derail your success.

Being your own boss sounds glamorous. You control your time, build your vision, and keep the profits. But behind the freedom lies a reality that often surprises new entrepreneurs. The truth is, there are hidden costs that can quietly eat away at your bottom line. The good news is you can spot these traps early and take steps to reduce them. Let’s look at the most common hidden costs of entrepreneurship and how to slash them before they derail your success.

1️⃣ Taxes You Did Not Plan For

When you are self employed, taxes are not taken out automatically. Forget to plan for them, and you could face a painful bill at year end.

Fix it: Open a separate savings account just for taxes and transfer a percentage of every payment you receive.

Dynamic Table: Suggested Tax Set Aside Rates

2️⃣ Health Insurance and Benefits

No employer means no benefits package. Health insurance, retirement contributions, and sick days all come out of your pocket.

Fix it: Shop around for a self employed health plan and build benefits into your pricing so you are not left short.

Dynamic Table: Monthly Benefit Costs to Expect

3️⃣ Tools and Technology Subscriptions

Software, apps, and platforms can add up quickly. That $29 subscription here and $15 there may seem small, but combined they drain cash every month.

Fix it: Audit your subscriptions quarterly and cancel tools you do not truly use.

Dynamic Table: How Small Subscriptions Add Up

4️⃣ Professional Services and Legal Fees

Lawyers, accountants, and consultants are vital, but their fees can surprise you.

Fix it: Budget for professional help in advance and shop around for flat fee services instead of paying high hourly rates.

Dynamic Table: Typical Annual Professional Costs

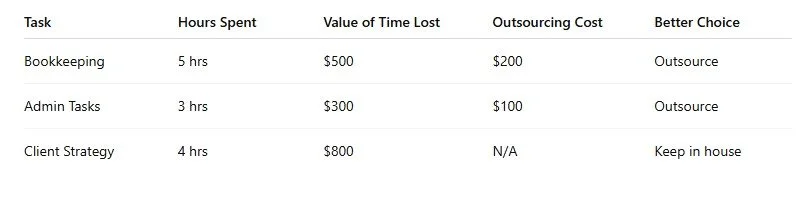

5️⃣ Opportunity Costs of Your Time

As your own boss, every hour has a price. Spending time on admin tasks or chasing late invoices is time you could have spent growing your business.

Fix it: Outsource low value tasks so you can focus on income generating work.

Dynamic Table: Time Value vs Outsourcing

The Bottom Line

The dream of being your own boss comes with hidden expenses that many do not expect. By planning for taxes, building in benefits, controlling subscriptions, budgeting for professional support, and protecting your time, you can keep more money in your pocket and grow smarter.

Managing these hidden costs of entrepreneurship will reduce stress, free up resources, and allow you to focus on building the business you love.

👉 Subscribe to Tea on the Ledger for more practical strategies and financial tips that help you master entrepreneurship.

How to Turn Your Side Hustle Into a 6-Figure Empire

Many people start a side hustle as a way to make a little extra cash. The idea of working for yourself, escaping the nine to five, and building something of your own is incredibly exciting. But how do you take your side hustle and scale it into a thriving six figure empire? The truth is, it is absolutely possible when you apply the right strategies. Today we will break down how to grow your side hustle to full time business step by step.

Many people start a side hustle as a way to make a little extra cash. The idea of working for yourself, escaping the nine to five, and building something of your own is incredibly exciting. But how do you take your side hustle and scale it into a thriving six figure empire? The truth is, it is absolutely possible when you apply the right strategies. Today we will break down how to grow your side hustle to full time business step by step.

🔴 1️⃣ Define Your Vision and Goals 🎯

A side hustle often begins casually, but to grow it into a real business you need clear goals. Ask yourself what success looks like. Do you want freedom, financial independence, or the chance to build a brand?

Table: Example Goals

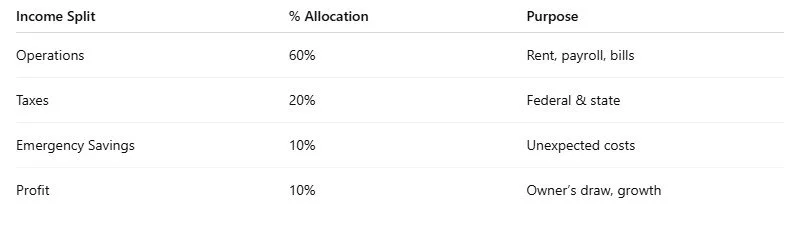

🟢 2️⃣ Build a Strong Financial Foundation 💵

Your business cannot grow if the money side is messy. Get serious about separating personal and business accounts, track expenses, and reinvest profits back into your business.

Table: Sample Budget Split

🔵 3️⃣ Focus on Scalable Income Streams 📈

A side hustle often starts with trading time for money. To scale, you need to create income streams that do not depend on you working every hour. This could include digital products, online courses, memberships, or outsourcing parts of your service.

Table: Examples of Scalable Income

🟣 4️⃣ Build Your Brand and Audience 📢

A full time business cannot exist without customers who trust you. Build a strong brand identity, show up consistently online, and share content that educates, entertains, or inspires your target market.

Table: Brand Growth Checklist

🟡 5️⃣ Know When to Go Full Time 🚀

Leaving your job too early can create stress, but waiting too long can hold you back. The sweet spot is when your side hustle income covers your living expenses or when your growth potential is limited by your nine to five hours.

Table: Decision Checkpoint

The Bottom Line

Your side hustle is more than just a part time project. With clear goals, smart money management, scalable income streams, and a growing brand, you can confidently make the leap and grow your side hustle to full time business.

👉 Subscribe to Tea on the Ledger for more practical strategies and financial tips that help you turn your hustle into a thriving empire.

The 5-Second Trick to Better Cash Flow (It’s So Simple!)

Cash flow problems can sneak up on small business owners fast. You make sales, but money seems to vanish before bills are paid. The truth is that healthy cash flow does not just happen, it is built through intentional habits. One of the smartest cash flow hacks for small businesses is what I call The Five Sessions Trick. It is a simple, structured way to keep your finances in order without adding stress to your week.

Cash flow problems can sneak up on small business owners fast. You make sales, but money seems to vanish before bills are paid. The truth is that healthy cash flow does not just happen, it is built through intentional habits. One of the smartest cash flow hacks for small businesses is what I call The Five Sessions Trick. It is a simple, structured way to keep your finances in order without adding stress to your week.

🔴 1️⃣ Session One: Review Incoming Cash 💵

The first step is always knowing what is coming in. Check your invoices, sales receipts, and pending payments. Spot late payers early so you can follow up before it turns into a crisis.

Table: Tracking Incoming Cash

🟢 2️⃣ Session Two: Check Outgoing Cash 💸

Next, look at what is leaving your bank. Bills, subscriptions, payroll, and vendor payments can quietly drain your balance if you are not watching.

Table: Outgoing Cash Commitments

🔵 3️⃣ Session Three: Balance the Two ⚖️

Now compare incoming with outgoing. If your payments do not line up with expenses, you will see cash flow dips before they happen.

Table: Cash Flow Balance Example

🟣 4️⃣ Session Four: Build a Cushion 🏦

Set aside a portion of your income into a savings account for taxes, emergencies, or uneven months. Even a ten percent buffer can be a lifesaver when clients pay late.

Table: Simple Allocation Example

🟡 5️⃣ Session Five: Forecast Ahead 📊

Finally, map out your next four weeks. Anticipating shortfalls gives you time to line up credit, cut costs, or speed up collections.

Table: Cash Flow Forecast Example

The Bottom Line

The Five Sessions Trick is a small commitment with a huge payoff. By carving out just a few short check ins each week, you will prevent nasty surprises, make smarter decisions, and finally get control over your cash flow.

Following these cash flow hacks for small businesses is about working smarter, not harder.

👉 Subscribe to Tea on the Ledger for more practical strategies and financial tips that keep your business thriving.

Why Your Business Bank Account is Draining Your Cash (Fix This Now) (Copy)

Running your business is stressful enough without your bank quietly eating away at your profits. Hidden fees, missed opportunities, and poor banking habits can all drain your hard-earned cash before you even notice. The good news? With a few simple business banking tips for entrepreneurs, you can stop your bank from bleeding you dry and start keeping more money where it belongs: in your pocket.

Running your business is stressful enough without your bank quietly eating away at your profits. Hidden fees, missed opportunities, and poor banking habits can all drain your hard-earned cash before you even notice. The good news? With a few simple business banking tips for entrepreneurs, you can stop your bank from bleeding you dry and start keeping more money where it belongs: in your pocket.

🔴 1️⃣ Stop Paying Unnecessary Fees 💸

Many banks sneak in charges for overdrafts, wire transfers, or falling below a minimum balance. These little “gotchas” can add up to hundreds or even thousands each year.

Fix it: Compare business checking accounts regularly. Look for fee-free accounts or negotiate with your bank. Yes, you can actually ask them to waive fees.

Fee Comparison Table

🟢 2️⃣ Separate Personal and Business Funds 🔑

If you are still running expenses through your personal account, your records are probably a mess and tax season becomes a horror film.

Fix it: Always maintain a dedicated business bank account. It protects your legal liability, keeps your books clean, and impresses potential lenders or investors.

🔵 3️⃣ Use Tech Friendly Banks 📲

Old school banks often charge extra for features, while modern fintech banks provide integrations with QuickBooks, PayPal, or Stripe at no additional cost.

Fix it: Switch to a bank that connects with your bookkeeping and payment systems. This saves you time, reduces errors, and lets you see your cash flow in real time.

Feature Comparison Table

🟣 4️⃣ Keep an Eye on Your Cash Flow 🔍

Entrepreneurs often focus on sales but forget to track money moving in and out. Poor cash flow management can lead to overdrafts, emergency loans, or even missed payroll.

Fix it: Set weekly reminders to review your transactions. Many banks offer dashboards and alerts. Make use of them.

🟡 5️⃣ Build a Banking Relationship 🤝

Your bank is not just where you park money, it can also be a partner in growth. Banks with strong small business support can offer lines of credit, merchant services, or even networking opportunities.

Fix it: Do not treat your banker like a stranger. Schedule a quarterly check in to review your needs and goals.

🟠 6️⃣ Automate Savings for Taxes and Emergencies 🏦

One of the biggest mistakes entrepreneurs make is forgetting Uncle Sam and unexpected expenses.

Fix it: Open a second business savings account. Automate transfers of 10 to 20 percent of income to cover taxes and rainy days. You will thank yourself when deadlines and surprises hit.

Savings Allocation Table

The Bottom Line

Your business bank account should support your growth, not quietly siphon off your profits. By following these business banking tips for entrepreneurs, you will protect your cash flow, simplify your finances, and build a stronger foundation for scaling your business.

👉 Subscribe to Tea on the Ledger for more practical strategies and financial tips that keep your business thriving.

Financial Mistakes New Business Owners Make—and How to Avoid Them

Starting a business is exciting. You’ve got your logo, your website, and a business plan scribbled on the back of a napkin. You’re ready to take on the world - until, a few months in, you realize your bank account looks like a sad meme and you’re asking yourself where did the money go?

Fear not, fellow entrepreneur. We’re diving into the financial mistakes new entrepreneurs make - so you can dodge them like a pro and keep your business (and your sanity) intact.

Let’s get into it.

Starting a business is exciting. You’ve got your logo, your website, and a business plan scribbled on the back of a napkin. You’re ready to take on the world - until, a few months in, you realize your bank account looks like a sad meme and you’re asking yourself where did the money go?

Fear not, fellow entrepreneur. We’re diving into the financial mistakes new entrepreneurs make - so you can dodge them like a pro and keep your business (and your sanity) intact.

Let’s get into it.

💸 Mistake #1: Mixing Personal and Business Finances

Ah yes, the classic “I’ll just pay for this business thing on my personal credit card and figure it out later” move. Spoiler: later never comes, and tax season becomes a full-blown horror movie.

How to Avoid It:

Open a separate business bank account now. Use it for everything - expenses, income, that one slightly questionable Canva subscription. Keep it clean, keep it separate.

🏦 Mistake #2: Underestimating Start-Up Costs

Sure, you can start a business on a shoestring budget… but “shoestring” doesn’t mean zero dollars. Many new business owners forget to budget for essentials like software, legal fees, insurance, and (oh yes) taxes.

How to Avoid It:

Write down all your expected costs, and then add 20%. Because surprise expenses will happen.

📊 Mistake #3: Not Tracking Cash Flow

Here’s a fun fact: cash flow is the lifeblood of your business. No cash flow, no business. Yet so many new entrepreneurs ignore it until their account is emptier than their fridge the day before payday.

How to Avoid It:

Track what’s coming in and going out. Use accounting software (QuickBooks, Wave, even a spreadsheet if you’re old school). Check it weekly - yes, every single week.

🧾 Mistake #4: Forgetting About Taxes

You know what’s worse than paying taxes? Paying taxes with penalties and interest because you didn’t plan ahead.

How to Avoid It:

Set aside 25%–30% of your income for taxes as it comes in. Better to have too much than not enough.

💰 Mistake #5: Underpricing Your Services

Here’s a tough pill to swallow: if you’re not charging enough, you’re not running a business - you’re running a charity. Many new entrepreneurs lowball their prices out of fear, only to realize they’re working for peanuts.

How to Avoid It:

Price based on your costs, desired profit, and the value you bring. Not sure how? Check out our blog on pricing services based on business finances (shameless plug, but hey, it’s helpful).

🚀 Mistake #6: Trying to Do It All Yourself

Just because you can do your own bookkeeping, marketing, website design, and social media doesn’t mean you should. Burnout is real, and doing everything can slow your business growth.

How to Avoid It:

Outsource where it makes sense - hire a bookkeeper (hello!), get a designer, or use that AI assistant you’ve been eyeing. Focus on what you do best.

😂 Mistake #7: Ignoring Your Financial Reports

If the words “profit and loss statement” make you want to take a nap, I get it. But ignoring your numbers is like driving blindfolded. You need to know what’s going on to make smart decisions.

How to Avoid It:

Review your reports monthly. Look at your profit, expenses, cash flow, and make a plan. You’ll feel like a boss, I promise.

🏁 Final Thoughts

Starting a business is a wild ride, but you don’t have to learn everything the hard way. By avoiding these common financial mistakes, you’ll set yourself up for smoother sailing and stronger profits.

So here’s your action plan:

✅ Keep personal and business finances separate

✅ Budget everything

✅ Track cash flow like your business depends on it (because it does)

✅ Plan for taxes

✅ Price for profit

✅ Get help when you need it

✅ Check your reports (and maybe pour a cup of tea while you’re at it)

👉 Want more tips, laughs, and real-talk finance advice for your small business? Subscribe to Tea on the Ledger - your go-to source for practical strategies, small business wisdom, and a healthy dose of humor.

Let’s make smart money moves, together. 🌿

How to Price Your Services Based on Your Finances

Ah, pricing. The eternal headache for every small business owner, side hustler, and “I swear I’m not winging it” entrepreneur. One minute you’re thinking, I’m worth a million bucks! and the next you’re Googling, Can I charge more than $5 for this service without scaring people off?

If you’ve ever wondered how to set prices that actually make you money (and not just “cover your coffee habit”), then you, my friend, are in the right place. Let’s talk about pricing services based on business finances - without making your brain melt.

Ah, pricing. The eternal headache for every small business owner, side hustler, and “I swear I’m not winging it” entrepreneur. One minute you’re thinking, I’m worth a million bucks! and the next you’re Googling, Can I charge more than $5 for this service without scaring people off?

If you’ve ever wondered how to set prices that actually make you money (and not just “cover your coffee habit”), then you, my friend, are in the right place. Let’s talk about pricing services based on business finances, without making your brain melt.

🧐 Why Bother Pricing Based on Finances?

Here’s the thing: if you don’t base your pricing on actual numbers, you’re basically throwing darts blindfolded. And spoiler alert: that’s how businesses end up broke by the end of the quarter.

Pricing based on your business finances helps you:

✅ Cover your costs (radical, I know)

✅ Pay yourself a real wage (because exposure doesn’t pay the bills)

✅ Plan for taxes, growth, and the occasional “treat yourself” moment

✅ Stop guessing and start growing

💡 The 5-Step Guide to Pricing Your Services Like a Pro

1️⃣ Know Your Costs (Yes, All of Them)

Start with the basics:

How much does it really cost you to deliver your service?

Are you including software, tools, subscriptions, and that “quick” Canva design you spent four hours on?

Don’t forget your time! If you’re working 12-hour days for pennies, we need to talk.

2️⃣ Set a Profit Goal (Because We’re Not a Charity)

Once you know your costs, add a profit margin. Yes, add. Profit is not optional.

Here’s a simple formula:

Cost of Service + Desired Profit = Price

Want a 20% profit margin? Cool. Charge 1.2 times your costs. Want to feel like a boss? Aim for 30%.

3️⃣ Look at the Market (But Don’t Obsess Over It)

Yes, it’s smart to see what others are charging. But don’t just copy your competitor’s prices because they look confident - chances are, they’re making the same mistakes.

Research to get a range, but price based on your actual business costs and goals.

4️⃣ Test It—Then Tweak It

Let’s be honest, pricing is a bit of trial and error. Set your price, see how the market responds, and adjust.

If clients run away screaming, maybe you’re too high (or you need to better explain your value). If they’re snapping up your services too easily, you might be leaving money on the table.

5️⃣ Review Regularly (Like, Every Quarter)

Your pricing isn’t set in stone, review it regularly! Check your financial reports, compare your profit margins, and adjust as your business grows.

If costs go up, guess what? So should your prices.

😂 Real Talk: Common Pricing Mistakes

Let’s take a moment to laugh (and cry) at some all-too-common pricing blunders:

❌ Charging “friend rates” for everyone (this is a business, not a charity)

❌ Forgetting about taxes, so that $500 invoice is really $400 after Uncle Sam takes his cut

❌ Pricing based on what you think clients will pay instead of what you need to earn

❌ Undercharging out of fear of rejection (newsflash: the right clients won’t flinch)

🏁 Final Thoughts

Pricing your services based on business finances isn’t just about making more money - it’s about making sure your business survives and thrives.

So here’s your action plan:

1️⃣ Calculate your costs

2️⃣ Add your profit margin

3️⃣ Review the market (briefly)

4️⃣ Test, tweak, repeat

5️⃣ Own your value, because you’re worth every penny

👉 For more finance tips that make sense (and maybe make you laugh a little), subscribe to Tea on the Ledger. We’ll send practical advice, strategies, and reminders that you can charge your worth - straight to your inbox.

Let’s make that money! 💰💪

What to Do if Your Business Is Losing Money

Running a business isn’t always sunshine, rainbows, and yacht parties. Sometimes it feels more like a leaky boat with you frantically bailing out water using a teaspoon. If your business is losing money and you’re wondering how to recover from business financial loss, you’re not alone, and you’re definitely not doomed.

Let’s break down the steps you can take to stop the bleeding, turn things around, and even have a laugh along the way (because let’s face it, crying into your Excel sheet won’t help).

Running a business isn’t always sunshine, rainbows, and yacht parties. Sometimes it feels more like a leaky boat with you frantically bailing out water using a teaspoon. If your business is losing money and you’re wondering how to recover from business financial loss, you’re not alone, and you’re definitely not doomed.

Let’s break down the steps you can take to stop the bleeding, turn things around, and even have a laugh along the way (because let’s face it, crying into your Excel sheet won’t help).

💸 First, Take a Deep Breath (and Look at the Numbers)

Before you spiral into panic mode, it’s time for a financial reality check. Open your books (yes, even the scary parts). Review your profit and loss statements, cash flow reports, and balance sheets.

Ask yourself:

✅ Where is the money going?

✅ Are there expenses that can be cut - like that subscription for a project management tool you haven’t logged into since 2022?

✅ Is your pricing too low?

✅ Are customers paying on time, or is your AR report a graveyard of unpaid invoices?

Facing the facts is the first step to fixing the problem.

🧹 Cut Costs (Without Cutting Corners)

You don’t need to go full-on Scrooge, but smart expense cuts can make a huge difference. Start by trimming the fat - look for unnecessary spending, renegotiate contracts, and consider switching to lower-cost tools that still get the job done.

Quick wins to consider:

Cancel underused software or services

Switch to a more affordable business bank account

Delay non-essential purchases

Outsource only what’s necessary

Think of it like a closet cleanout - if it’s not sparking joy (or revenue), it might need to go.

📈 Boost Revenue (Yes, Easier Said Than Done, But Let’s Talk)

Cutting costs can only take you so far. To truly recover from financial loss, you need to find ways to increase your income.

Here’s how:

💡 Raise prices (gently, explain the value!)

💡 Introduce a new service or product

💡 Upsell or cross-sell existing clients

💡 Follow up on unpaid invoices like your rent depends on it (because, let’s be honest, it kinda does)

And remember: sometimes a small pivot can bring in big results.

🏦 Get Help Before It’s Too Late

If the hole feels too deep, it’s okay to ask for help. This could mean:

Talking to a bookkeeper (ahem, like me!)

Meeting with a financial advisor

Discussing financing options with your bank

Applying for a small business loan or grant

Remember, even the most successful businesses have faced losses. The key is to tackle it early.

🌟 Plan for the Future (Because You’re Not Giving Up That Easy)

Once you’ve stabilized, create a plan to avoid the same mess next year. Set a budget, track key metrics (like cash flow and profit margins), and review your finances regularly.

Pro tip: Schedule a monthly finance date with yourself. Grab a coffee (or a glass of wine, no judgment), review your numbers, and adjust as needed.

💬 Final Thoughts: You’re Not Alone, and You’re Stronger Than You Think

Losing money in business happens. It doesn’t mean you’re bad at what you do, and it definitely doesn’t mean you should throw in the towel. It means you’re human, and every successful entrepreneur has been there.

So take a breath, make a plan, and get back in the game.

👉 Want more practical, no-nonsense tips for managing your business finances (with a side of humor)? Subscribe to Tea on the Ledger for insights that make bookkeeping a little less boring and your business a lot more profitable.

How to Project Your Business Finances for the Year Ahead

Ever feel like you are guessing when it comes to your business finances?

You are not alone. Many small business owners and freelancers find forecasting tricky, but a good business finance forecasting guide can change everything.

When you forecast your income, expenses, and cash flow for the year ahead, you gain clarity, confidence, and control over your financial future. Let’s break down the process step by step - without the jargon.

Ever feel like you are guessing when it comes to your business finances?

You are not alone. Many small business owners and freelancers find forecasting tricky, but a good business finance forecasting guide can change everything.

When you forecast your income, expenses, and cash flow for the year ahead, you gain clarity, confidence, and control over your financial future. Let’s break down the process step by step, without the jargon.

📊 What is Business Finance Forecasting?

Business finance forecasting is the process of estimating your future financial performance. It is not just about making random guesses; it is about creating a roadmap for your business based on past data, current trends, and realistic assumptions.

A forecast helps you answer key questions:

How much will I earn?

What will I spend?

Will I have enough cash to cover expenses?

Can I afford to invest in growth?

🏗️ Your Step-by-Step Business Finance Forecasting Guide

Here is a simple system for forecasting your finances for the year ahead.

1️⃣ Review Your Past Numbers

Look at your last 12 months of financial data:

✅ Total revenue

✅ Total expenses

✅ Profit margins

✅ Seasonal trends (busy and slow periods)

This helps you spot patterns and create a realistic starting point.

2️⃣ Project Your Revenue

Based on your past data and future plans:

Estimate how much you will earn each month.

Consider new products, services, or clients you expect to add.

Be realistic, factor in potential challenges.

For example:

If you earned $10,000 per month last year and plan to launch a new service, you might forecast $12,000 per month for the next year.

3️⃣ Forecast Your Expenses

List out fixed expenses (like rent, software subscriptions) and variable expenses (like supplies, marketing, or hourly labor).

Ask:

Will any costs increase this year?

Are there new expenses to include?

Can you cut any unnecessary costs?

Create a monthly estimate for each category.

4️⃣ Map Out Your Cash Flow

Even if you expect to be profitable, you might still face cash flow issues. A cash flow forecast helps you predict when money will come in and when it will go out.

Consider:

✅ Payment terms (when clients actually pay)

✅ Seasonal dips

✅ Large expenses due (like taxes or equipment)

This step keeps your business prepared, not surprised.

5️⃣ Set Financial Goals and Milestones

Once you have your forecast, set clear goals:

✅ Monthly revenue targets

✅ Expense limits

✅ Profit margin goals

✅ Savings targets (for taxes, emergencies, or growth)

These goals help you measure success and stay on track.

💡 Why Business Finance Forecasting Matters

A good forecast helps you:

✅ Make informed decisions

✅ Avoid cash flow problems

✅ Plan for taxes and big expenses

✅ Invest in growth with confidence

Without a forecast, you are just hoping for the best. With a forecast, you are creating a plan for success.

📅 How Often Should You Update Your Forecast?

Review and adjust your forecast monthly or quarterly. Business is dynamic - your forecast should be too.

✅ If sales are up, update your projections.

✅ If a major client drops off, adjust your forecast.

✅ If expenses change, reflect it in your plan.

Final Thoughts

This business finance forecasting guide gives you a clear, step-by-step approach to projecting your income, expenses, and cash flow for the year ahead.

No more guesswork - just solid numbers to guide your decisions.

Ready to take control of your business finances? Let’s make this your best year yet.

What Your Profit & Loss Statement Should Really Tell You

If you have ever stared at your Profit and Loss Statement (P&L) and thought, “What am I actually looking at?”, you are not alone.

Many freelancers, side hustlers, and small business owners struggle with understanding profit and loss statement details - yet this simple document can give you a crystal-clear picture of your business’s financial health.

Let’s break it down, step by step, so you can stop guessing and start using your P&L like a pro.

If you have ever stared at your Profit and Loss Statement (P&L) and thought, “What am I actually looking at?”, you are not alone.

Many freelancers, side hustlers, and small business owners struggle with understanding profit and loss statement details, yet this simple document can give you a crystal-clear picture of your business’s financial health.

Let’s break it down, step by step, so you can stop guessing and start using your P&L like a pro.

📊 What is a Profit and Loss Statement?

A Profit and Loss Statement (sometimes called an Income Statement) is a summary of your business’s revenue, costs, and profits over a specific period - usually a month, quarter, or year.

It shows:

✅ How much you earned (revenue)

✅ How much you spent (expenses)

✅ What is left over (profit or loss)

In other words, it tells you: Did your business make money or lose money?

🧩 The Key Sections of a Profit and Loss Statement

Here is what you will typically find on a P&L:

✅ Revenue (or Sales): The total income from your products or services.

✅ Cost of Goods Sold (COGS): The direct costs to produce what you sell (like materials or labor).

✅ Gross Profit: Revenue minus COGS, this shows how much you made before other expenses.

✅ Operating Expenses: The regular costs of running your business (rent, software, marketing).

✅ Net Profit (or Net Loss): What is left after all expenses are paid, this is the bottom line.

💡 What Should Your P&L Really Tell You?

Your Profit and Loss Statement is not just a list of numbers. It is a story about your business. Here is what you should be looking for:

1️⃣ Are You Actually Profitable?

Look at your Net Profit. Are you consistently making a profit, or are you running at a loss?

If your net profit is too low (or negative), it is a sign to review your pricing, cut costs, or find ways to increase revenue.

2️⃣ How Much Does It Cost to Run Your Business?

Your Operating Expenses section shows where your money is going. Are there areas where you can save?

For example:

Are subscriptions piling up?

Can you negotiate better rates with suppliers?

Is your marketing spend delivering results?

3️⃣ What are Your Profit Margins?

Calculate your Gross Profit Margin:

This tells you how much money you are making from sales after covering production costs.

Higher margins = more room to invest in growth or pay yourself more.

4️⃣ Are There Seasonal or Monthly Trends?

Review your P&L over several months. Are there patterns?…..like slow summers or a busy holiday season?

Spotting trends helps you plan for cash flow dips and set realistic revenue targets.

🛠️ How to Use Your P&L for Better Decisions

✅ Pricing: Are your prices too low to cover costs?

✅ Spending: Where can you cut back without hurting your business?

✅ Investments: Can you afford that new hire, software, or marketing push?

✅ Taxes: Are you setting enough aside for quarterly taxes?

Your P&L is not just for your accountant, it is for you to make smarter choices every month.

📅 How Often Should You Review Your P&L?

Once a year at tax time is not enough.

Review your Profit and Loss Statement monthly. This keeps you informed, agile, and able to course-correct quickly if needed.

Final Thoughts

Understanding profit and loss statement basics is a skill every business owner should master. It is not just numbers on a page……it is the financial story of your business.

By reviewing your P&L regularly and asking the right questions, you will make better decisions, protect your cash flow, and build a stronger, more profitable business.

Let’s make your finances work for you, not against you.

Should You Open a Business Savings Account? Yes…..Here’s Why

When you’re running a small business, every dollar counts. You might already have a business checking account to handle day-to-day transactions, but here’s the question:

Should you open a business savings account, too?

The answer is a resounding yes - and here’s why.

Let’s break down the benefits of business savings account setups and how they can protect your business, fuel your growth, and keep you ready for whatever comes next.

When you’re running a small business, every dollar counts. You might already have a business checking account to handle day-to-day transactions, but here’s the question:

Should you open a business savings account, too?

The answer is a resounding yes - and here’s why.

Let’s break down the benefits of business savings account setups and how they can protect your business, fuel your growth, and keep you ready for whatever comes next.

💡 What is a Business Savings Account?

A business savings account is like a personal savings account, but for your business. It’s a dedicated place to park cash reserves, separate from your everyday operating funds.

Unlike a checking account, a savings account:

✅ Earns interest on your balance

✅ Has limited withdrawals per month (by design, to help you save)

✅ Encourages you to build a financial buffer for your business

💰 The Top Benefits of Business Savings Account

1️⃣ Protect Your Cash Flow

Every business faces ups and downs. Whether it’s a slow sales month, an unexpected expense, or a late client payment, a business savings account acts as your safety net.

It helps you:

Cover payroll during lean times

Handle emergency repairs

Weather seasonal slumps

Without dipping into personal funds or relying on credit cards.

2️⃣ Build an Emergency Fund

You never know when a surprise expense will hit - think equipment breakdowns, legal fees, or sudden market changes.

By regularly setting aside a portion of your profits into a business savings account, you create a financial cushion that helps you stay prepared and in control.

3️⃣ Earn Interest on Idle Funds

Let’s be real: letting your extra business cash sit in a non-interest-bearing checking account is like leaving money on the table.

Many business savings accounts offer competitive interest rates (even more if you shop around for high-yield options).

That means your money works for you, earning passive income while you focus on growing your business.

4️⃣ Plan for Taxes & Big Expenses

Tax season doesn’t have to be stressful when you’re prepared. A business savings account is the perfect place to set aside funds for:

Quarterly estimated taxes

Annual tax payments

Large purchases (equipment, software, etc.)

With your savings separate from your day-to-day funds, you won’t accidentally spend what you need for taxes or other big bills.

5️⃣ Show Financial Responsibility

If you’re applying for a loan, seeking investors, or working with vendors, having a business savings account demonstrates financial discipline.

It shows you’re planning ahead, managing risk, and running your business like a pro - qualities that build trust and credibility.

🔑 How to Get Started

Opening a business savings account is simple:

✅ Choose a bank or credit union that offers business accounts

✅ Compare interest rates, fees, and minimum balance requirements

✅ Provide your business formation documents (LLC, EIN, etc.)

✅ Fund your account and set a goal (e.g., 10% of monthly revenue goes to savings)

Pro tip: Automate transfers from your business checking to savings to make it effortless.

Final Thoughts

The benefits of business savings account are clear:

✅ Protect your cash flow

✅ Build an emergency fund

✅ Earn passive income

✅ Stay tax-ready

✅ Show you mean business

If you’re ready to future-proof your finances and reduce money stress, it’s time to open that business savings account.

Small steps today lead to big rewards tomorrow. Let’s make it happen!

Financial Red Flags That Scare Away Investors

Picture this: you’ve got a big pitch meeting lined up. You’re ready to wow potential investors with your vision, your product, and your passion.

But here’s the catch - even the best ideas won’t get funded if your business finances throw up red flags.

Whether you’re a freelancer looking for a small capital injection, or a small business owner seeking a major investment, knowing the business finance red flags for investors is critical.

Let’s dive into the most common financial warning signs that can make investors hesitate, and how you can fix them before they kill your funding dreams.

Picture this: you’ve got a big pitch meeting lined up. You’re ready to wow potential investors with your vision, your product, and your passion.

But here’s the catch - even the best ideas won’t get funded if your business finances throw up red flags.

Whether you’re a freelancer looking for a small capital injection, or a small business owner seeking a major investment, knowing the business finance red flags for investors is critical.

Let’s dive into the most common financial warning signs that can make investors hesitate, and how you can fix them before they kill your funding dreams.

🚩 1️⃣ Messy or Incomplete Financial Records

Investors love clarity - and they expect your numbers to be clean, complete, and easy to understand.

If your books are disorganized, missing key reports, or rely on guesstimates, it’s a major red flag. Investors will think:

“How can they manage money if they can’t even track it?”

“What else are they missing?”

How to fix it:

✅ Use accounting software (like QuickBooks, Xero, or Wave).

✅ Keep financial statements up to date: P&L, balance sheet, cash flow.

✅ Be ready to explain your numbers clearly and confidently.

🚩 2️⃣ Inconsistent Cash Flow

Investors look for businesses with predictable cash flow, because it signals stability.

If your cash flow shows huge swings month-to-month with no clear explanation, they’ll wonder:

“Is this business too risky?”

“Can they cover operating expenses consistently?”

How to fix it:

✅ Build a cash flow forecast (even a simple spreadsheet works).

✅ Explain seasonal trends or one-off events that cause fluctuations.

✅ Have a plan for smoothing cash flow (like offering retainer packages or recurring revenue models).

🚩 3️⃣ High Debt with No Clear Repayment Plan

Debt itself isn’t a deal-breaker, but uncontrolled debt with no plan to manage it? Major red flag.

Investors want to know:

How much debt do you have?

What’s it used for?

What’s the repayment schedule?

How to fix it:

✅ Be transparent about your debt and how you’re managing it.

✅ Show that debt is being used for growth, not to plug holes.

✅ Highlight strategies to reduce or restructure debt over time.

🚩 4️⃣ Low or Negative Profit Margins

If your business isn’t making a profit, or if margins are razor-thin - investors may wonder if the business is sustainable.

How to fix it:

✅ Break down your cost structure and show you know where every dollar goes.

✅ Highlight strategies to improve margins (raising prices, cutting costs, increasing efficiency).

✅ Share a timeline for profitability - investors love a clear, realistic plan.

🚩 5️⃣ Unclear or Unrealistic Financial Projections

Wild revenue forecasts with no supporting data = 🚩.

Investors will ask:

“How did you come up with these numbers?”

“Are these projections based on facts or wishful thinking?”

How to fix it:

✅ Use data-driven assumptions - industry benchmarks, past performance, market research.

✅ Provide best-case, worst-case, and realistic projections.

✅ Be prepared to walk through your assumptions in detail.

🚩 6️⃣ Personal Finances Mixed with Business Finances

Blurring the lines between personal and business money is a surefire way to make investors nervous.

It suggests poor financial management, and raises concerns about legal and tax compliance.

How to fix it:

✅ Open separate business bank accounts and credit cards.

✅ Pay yourself a salary from the business, rather than making random transfers.

✅ Keep clean, separate records for business vs. personal expenses.

Final Thoughts

Understanding the business finance red flags for investors is your secret weapon for building trust and securing funding.

By cleaning up your books, managing cash flow, keeping debt in check, and making realistic projections, you’ll not only impress investors - you’ll also set your business up for long-term success.

Understanding Business Credit Scores (And Why They Matter)

Ever tried applying for a business loan or credit card and wondered why you got denied or approved for way less than you needed?

Chances are, it had something to do with your business credit score.

Your personal credit score is important, sure - but for your business, building credit is a whole different ball game.

Let’s break down exactly what a business credit score is, why it matters, and how to build business credit score from scratch (even if you’re a freelancer, side hustler, or small business owner just getting started).

Ever tried applying for a business loan or credit card and wondered why you got denied or approved for way less than you needed?

Chances are, it had something to do with your business credit score.

Your personal credit score is important, sure, but for your business - building credit is a whole different ball game.

Let’s break down exactly what a business credit score is, why it matters, and how to build business credit score from scratch (even if you’re a freelancer, side hustler, or small business owner just getting started).

💼 What Is a Business Credit Score, Anyway?

Think of it as your business’s financial reputation.

Lenders, vendors, and even potential partners use it to decide:

✅ Whether to give you credit

✅ How much to lend you

✅ What interest rates to offer

✅ How much risk you represent

Your business credit score typically ranges from 0 to 100 (unlike personal scores, which go up to 850). The higher the score, the better.

🌟 Why Does Your Business Credit Score Matter?

Here’s why you should care:

Access to Funding: A good score helps you qualify for loans, credit cards, and lines of credit.

Better Terms: Lower interest rates and higher credit limits.

Supplier Relationships: Some vendors check your score before offering payment terms like Net-30.

Business Growth: With credit, you can invest in tools, marketing, and team members without draining your cash flow.

🏗️ How to Build Business Credit Score: Step-by-Step

Ready to level up your financial game? Here’s how to build business credit score that works for you:

1️⃣ Set Up Your Business Properly

✅ Register your business (LLC, Corp, etc.)

✅ Get an EIN (Employer Identification Number) from the IRS

✅ Open a business bank account in your business’s name

This creates separation between you and your business, a key first step for building credit.

2️⃣ Get a D-U-N-S Number

Dun & Bradstreet is one of the main credit bureaus for businesses. You’ll need a D-U-N-S number (it’s free!) to start your business credit profile.

Apply here: Dun & Bradstreet

3️⃣ Open Business Accounts That Report to Credit Bureaus

Start small:

Business credit cards (e.g., Capital One Spark, Amex Blue Business)

Vendor accounts with Net-30 terms (e.g., Uline, Grainger, Quill)

Business loans or lines of credit (if eligible)

Make small purchases, pay on time (or early!), and build your score over time.

4️⃣ Pay Everything On Time (Or Early)

This is the golden rule. Your payment history is the biggest factor in your business credit score.

Even one late payment can tank your score - so set up reminders, automate payments, or use accounting software to stay on top of due dates.

5️⃣ Monitor Your Business Credit Regularly

Stay in the loop by checking your reports at:

Dun & Bradstreet

Experian Business

Equifax Business

Look for errors, outdated info, or missing accounts. Catching issues early = a healthier score.

🚀 Quick Wins to Boost Your Score

✅ Keep credit utilization low (use less than 30% of your limit)

✅ Don’t close old accounts (long history = better score)

✅ Ask vendors to report your good payment history

✅ Build a strong relationship with your bank

Final Thoughts

Your business credit score is more than just a number - it’s your ticket to growth, flexibility, and financial freedom.

By learning how to build business credit score the right way, you’re giving your business a foundation for success.

Ready to take action? Start with small steps today - and watch your financial future get brighter.

How to Build a Cash Reserve for Your Business

If you’ve ever had an unexpected expense hit your business - like a client paying late, an equipment breakdown, or a slow sales month, you know how quickly a cash flow crunch can turn into a full-blown crisis.

That’s why every business needs an emergency fund.

Whether you’re a solo freelancer, a side hustler, or running a small team, learning how to build a business emergency fund is a game-changer.

Let’s break it down step-by-step so you can protect your business from the unexpected - and sleep better at night.

If you’ve ever had an unexpected expense hit your business - like a client paying late, an equipment breakdown, or a slow sales month, you know how quickly a cash flow crunch can turn into a full-blown crisis.

That’s why every business needs an emergency fund.

Whether you’re a solo freelancer, a side hustler, or running a small team, learning how to build a business emergency fund is a game-changer.

Let’s break it down step-by-step so you can protect your business from the unexpected, and sleep better at night.

💡 What’s a Business Emergency Fund, Anyway?

Think of it as your business’s financial safety net. It’s cash you set aside to cover:

✅ Unplanned expenses (repairs, legal fees, refunds)

✅ Gaps in revenue (late payments, slow months)

✅ Temporary setbacks (illness, supply chain delays)

This isn’t just a nice-to-have - it’s a must-have if you want your business to survive and thrive long-term.

📊 How Much Should You Save?

The general rule of thumb for a business emergency fund is:

✅ 3–6 months of operating expenses

If that feels like a lot, start small. Even one month’s expenses is better than nothing.

Ask yourself:

What are my fixed monthly costs (rent, payroll, software)?

What’s the minimum I need to stay afloat?

Example:

Monthly expenses: $5,000

3-month emergency fund target: $15,000

💸 Step-by-Step: How to Build a Business Emergency Fund

1️⃣ Start with a Budget

You can’t save what you don’t know.

Review your monthly expenses

Identify non-essentials to cut or reduce

Allocate a percentage of profits toward your fund (even 5–10% helps!)

2️⃣ Open a Separate Business Savings Account

Keep your emergency fund out of your day-to-day account to avoid accidental spending.

Look for:

✅ No or low fees

✅ Interest-bearing options

✅ Easy transfers

3️⃣ Set a Savings Goal & Automate It

Decide how much you’ll save each month, then automate it.

Example:

Save $500/month = $6,000 in a year

Save $1,000/month = $12,000 in a year

Small, steady deposits add up faster than you think.

4️⃣ Treat It Like a Non-Negotiable Bill

Your emergency fund is as important as your rent or utilities.

Build it into your budget and don’t dip into it unless it’s truly an emergency.

5️⃣ Replenish After You Use It

If you need to tap into your fund, no shame! That’s what it’s there for.

But once you’ve used it, make a plan to rebuild it - even if it’s just a little each month.

🚀 Why This Matters

Emergencies happen. Clients ghost you. The market slows. Stuff breaks.

Having a business emergency fund means you won’t have to:

❌ Swipe your personal credit card

❌ Take out a loan with high interest

❌ Stress about making payroll

It’s financial peace of mind - so you can focus on growing your business, not scrambling for cash.

Final Thoughts

Building an emergency fund is one of the smartest, most practical steps you can take for your business.

Start small. Stay consistent. And remember - it’s not about perfection, it’s about progress.

5 Signs You Need Help With Your Business Finances

Let’s be real, running a business is tough, and staying on top of your finances? Even tougher.

If you’ve been feeling overwhelmed, unsure if you’re making a profit, or just winging it when it comes to taxes and cash flow, you’re not alone. But here’s the thing: ignoring money problems won’t make them go away - it’ll just make them harder to fix later.

So how do you know when it’s time to stop DIYing your books and get some expert help?

Here are 5 clear signs your business needs financial help, and what to do about it.

Let’s be real - running a business is tough, and staying on top of your finances? Even tougher.

If you’ve been feeling overwhelmed, unsure if you’re making a profit, or just winging it when it comes to taxes and cash flow, you’re not alone. But here’s the thing: ignoring money problems won’t make them go away, it’ll just make them harder to fix later.

So how do you know when it’s time to stop DIYing your books and get some expert help?

Here are 5 clear signs your business needs financial help, and what to do about it.

🚩 1. You Don’t Know if You’re Profitable

Let’s start with the big one: Are you making money or not?

If you don’t know your profit margins, can’t say what your top-selling products or services are, or aren’t sure how much cash you’ll have at the end of the month - that’s a red flag.

👉 Solution:

Get a clear view of your numbers. A bookkeeper or accountant can help you set up simple reports (like a P&L and cash flow statement) so you always know where you stand.

🚩 2. Your Cash Flow Feels Like a Roller Coaster

One month, you’re flush with cash. The next? You’re scrambling to pay bills.

Inconsistent cash flow is one of the top signs your business needs financial help, and it’s a major reason businesses fail.

👉 Solution:

A finance pro can help you create a cash flow forecast, manage payment terms, and even set up strategies like payment plans or deposits to smooth out the ups and downs.

🚩 3. Tax Season Feels Like a Nightmare

If you’re panicking every April (or worse, filing extensions because you’re unprepared), it’s time to get proactive.

👉 Solution:

A bookkeeper can keep your records organized year-round, so tax time becomes a breeze. They’ll help you track deductible expenses, file on time, and even save money by spotting tax-saving opportunities you might miss.

🚩 4. You’re Too Busy to Manage Your Finances

If you’re spending more time on client work or growing your business (great!) but neglecting your books (not so great), it’s time to delegate.

👉 Solution:

Your time is valuable. A financial expert can handle the day-to-day numbers, so you can focus on what you do best - running your business.

🚩 5. Your Business Is Growing, but Your Finances Aren’t

If your revenue is up but your bank balance isn’t, something’s off. This is one of the most common, and most overlooked signs your business needs financial help.

👉 Solution:

You may need better pricing strategies, cost controls, or financial planning. An expert can help you create a roadmap for sustainable growth.

Final Thoughts

Don’t wait for a financial crisis to get help. If any of these signs sound familiar, it’s time to take action.

The sooner you organize your finances, the sooner you’ll feel confident, in control, and ready to grow.

The Best Way to Organize Your Business Receipts

Let’s face it: tracking down business receipts during tax season is the WORST. You know you bought that printer ink, but where’s the proof? That client lunch? Buried somewhere in your inbox.

Organizing business receipts for taxes isn’t just about staying neat - it’s about saving money, avoiding headaches, and keeping the IRS happy.

The good news? You don’t need a fancy system or expensive software. Just a simple, consistent method that works for you.

Here’s exactly how to organize your business receipts like a pro, without spending hours on paperwork.

Let’s face it: tracking down business receipts during tax season is the WORST. You know you bought that printer ink, but where’s the proof? That client lunch? Buried somewhere in your inbox.

Organizing business receipts for taxes isn’t just about staying neat - it’s about saving money, avoiding headaches, and keeping the IRS happy.

The good news? You don’t need a fancy system or expensive software. Just a simple, consistent method that works for you.

Here’s exactly how to organize your business receipts like a pro, without spending hours on paperwork.

🚀 Why Organizing Business Receipts Matters

💡 Fun fact: The IRS requires businesses to keep proof of expenses. If you can’t show it, you risk losing out on deductions, or worse - facing an audit.

A good receipt system helps you:

✅ Maximize tax deductions

✅ Make bookkeeping easier

✅ Stay stress-free at tax time

✅ Prove your case if audited

So, let’s make it simple.

🗂️ Step 1: Choose Your System (Digital or Paper)

First, decide:

Digital receipts: Scan or save PDF copies

Paper receipts: Store them in folders, envelopes, or binders

📲 Pro Tip: Go digital whenever possible. Apps like QuickBooks, Dext, or Expensify make it easy to snap photos and auto-organize receipts.

📸 Step 2: Scan and Save Receipts Immediately

Don’t let receipts pile up. As soon as you get one:

Snap a picture

Upload it to your app, cloud folder (Google Drive, Dropbox), or bookkeeping software

Add a note: client name, expense type, and date

Even if you keep paper copies, back them up digitally for peace of mind.

🗃️ Step 3: Organize by Category

For tax season, sort receipts into categories that match your tax forms:

Office Supplies

Travel & Meals

Marketing

Equipment & Assets

Software & Subscriptions

Client Expenses

Miscellaneous

This makes it super easy to tally deductions later.

💸 Step 4: Keep Receipts for the Right Length of Time

For tax purposes, the IRS recommends:

3 years for most tax records

7 years if you claim a loss or deductions related to bad debt

So, make a habit of archiving old receipts once a year, but don’t toss them too soon!

🔒 Step 5: Secure Your Records

Back up your files in the cloud or on an external hard drive.

For physical receipts:

Use folders labeled by year and category

Keep them in a safe, dry place

Your future self (and your accountant) will thank you.

🏆 Bonus Tip: Create a Monthly Receipt Routine

Set a recurring calendar reminder:

10 minutes each week: Snap & file new receipts

30 minutes monthly: Review and categorize

Consistency = no chaos at tax time.

Final Thoughts

Organizing business receipts for taxes doesn’t have to be a chore. With the right system, and a little discipline, you’ll stay tax-ready, stress-free, and in control of your finances.

How to Separate Business and Personal Finances

Running a business is tough enough without the added stress of mixing personal and business finances. If you’ve ever wondered why your bookkeeping feels like a jumbled mess, or why tax season makes you want to pull your hair out - you’re not alone.

Here’s the thing: separating your business and personal finances is one of the smartest moves you can make. It’s not just about being organized (though that’s a huge bonus) - it’s about protecting your business, simplifying your taxes, and running your finances like a pro.

So, let’s break down exactly how to separate business and personal finances, step by step.

Running a business is tough enough without the added stress of mixing personal and business finances. If you’ve ever wondered why your bookkeeping feels like a jumbled mess, or why tax season makes you want to pull your hair out - you’re not alone.

Here’s the thing: separating your business and personal finances is one of the smartest moves you can make. It’s not just about being organized (though that’s a huge bonus) - it’s about protecting your business, simplifying your taxes, and running your finances like a pro.

So, let’s break down exactly how to separate business and personal finances, step by step.

🚧 Why Separating Finances Matters

Before we dive in, let’s get real for a second:

💡 Mixing your personal and business money is risky.

You could:

Miss out on tax deductions

Struggle with cash flow

Face IRS scrutiny or legal headaches

Blur the lines between your business and personal liability

Bottom line? A little organization now saves a lot of stress later.

✅ Step 1: Open a Business Bank Account

This is your non-negotiable first step. Even if you’re a solo freelancer or side hustler, a dedicated business bank account is a must.

Why?

It keeps your income and expenses cleanly separated

It helps you track cash flow

It makes tax time a breeze

Bonus points: Get a business debit card for easy access and to build your business credit.

✅ Step 2: Set Up a Business Credit Card (Optional but Powerful)

Once your business account is set, consider a business credit card. This:

Keeps business expenses in one place

Helps you earn rewards or cashback

Builds credit history for your business

Just remember: Only use it for business. No sneaky Starbucks runs unless it’s for a client meeting!

✅ Step 3: Pay Yourself a Salary (Even If It’s Small)

Treat yourself like an employee.

Decide on a set amount you’ll “pay” yourself from your business account each month

Transfer it to your personal account

Don’t dip into business funds randomly for personal spending

This creates clear lines between you and your business, helping with budgeting and tax planning.

✅ Step 4: Track Your Business Expenses Diligently

Use software (like QuickBooks, Wave, or a simple spreadsheet) to track business income and expenses.

Include:

Office supplies

Marketing costs

Software subscriptions

Client meals (but be careful with IRS rules!)

If it’s a business cost, log it in your business records - not your personal ones.

✅ Step 5: Keep Proof (Receipts, Invoices, and All That Good Stuff)

Back up your expenses with documentation:

Save digital or physical copies of receipts

Keep invoices organized

Store everything in a cloud folder (Google Drive, Dropbox)

This protects you during tax time and if you’re ever audited.

✅ Step 6: Review Regularly (Don’t Let It Slide!)

Schedule a monthly money date with yourself. Review:

Business income

Business expenses

Personal spending

The more consistent you are, the less messy your books become - and the less likely you’ll mix funds.

Final Thoughts

How to separate business and personal finances isn’t rocket science, but it does take discipline.

Start with a business bank account, pay yourself like a boss, and stay organized. Your future self (and your accountant) will thank you.

Top 10 Business Finance Apps That Actually Save You Time

Let’s face it, running a business is hard enough without wasting hours managing your finances. The good news? There are apps built specifically to make money management faster, easier, and even kind of enjoyable.

Whether you're a freelancer, solopreneur, or small business owner, the best apps for business finances in 2025 help you stay on top of income, expenses, taxes, and more - with minimal effort.

Here are 10 apps worth checking out if you want to spend less time crunching numbers and more time growing your business.

Let’s face it, running a business is hard enough without wasting hours managing your finances. The good news? There are apps built specifically to make money management faster, easier, and even kind of enjoyable.

Whether you're a freelancer, solopreneur, or small business owner, the best apps for business finances in 2025 help you stay on top of income, expenses, taxes, and more - with minimal effort.

Here are 10 apps worth checking out if you want to spend less time crunching numbers and more time growing your business.

1. QuickBooks Online

Best for: All-in-one accounting for small businesses

QuickBooks remains the gold standard for cloud accounting. It automates invoicing, tracks expenses, manages payroll, and integrates with nearly every tool you use.

Why it saves you time:

Bank syncing for real-time updates

Built-in tax tools

Recurring invoices and reports

✅ Bonus: Clean dashboards and mobile-friendly design

2. FreshBooks

Best for: Service-based businesses and freelancers

FreshBooks is loved for its user-friendly interface and simple invoicing. It also offers time tracking, expense management, and client communication tools.

Why it saves you time:

Track time, send invoices, and accept payments in one place

Automated late payment reminders

Mileage tracking for easy deductions

3. Xero

Best for: Businesses with global operations or multiple users

Xero offers powerful accounting features with great scalability. It's perfect for growing teams and works seamlessly with over 1,000 third-party apps.

Why it saves you time:

Bulk reconciliation of bank transactions

Real-time collaboration with bookkeepers

Multi-currency support

4. Wave

Best for: Budget-conscious entrepreneurs

Wave is a free accounting solution with surprisingly robust features. It covers invoicing, payments, and basic bookkeeping - perfect for early-stage businesses.

Why it saves you time:

Automated expense tracking

Seamless bank integration

No fees for core features

5. Expensify

Best for: Expense tracking and reimbursements

Expensify is ideal for business owners or teams who travel or spend on behalf of the company. Snap a picture of a receipt, and it’s instantly logged and categorized.

Why it saves you time:

One-tap expense reports

SmartScan for receipts

Company card syncing

6. Bonsai

Best for: Freelancers and creatives

Bonsai is more than finance, it’s a full freelance business suite. But its expense tracking and tax estimates are fantastic if you want to manage everything in one place.

Why it saves you time:

Auto-import expenses

Pre-filled tax estimates

Contracts and invoices included

7. Zoho Books

Best for: Small businesses wanting customization

Zoho Books is part of the larger Zoho ecosystem. It’s a powerful, flexible option with tons of automation and customization options.

Why it saves you time:

Auto-scheduling of recurring transactions

Smart dashboards and insights

Built-in time tracking and project billing

8. Float

Best for: Cash flow forecasting

Float connects to your accounting software to give you real-time cash flow projections. It’s a game-changer if you want to plan smarter.

Why it saves you time:

Visual, forward-looking insights

What-if scenario planning

Real-time sync with QuickBooks, Xero, and FreeAgent

9. Pleo

Best for: Team expense management

Pleo is perfect for teams. It offers smart company cards and automates expense reports, no more chasing receipts or mystery charges.

Why it saves you time:

Auto-categorization of team expenses

Instant spending visibility

Set card limits and control spending in real time

10. Hurdlr

Best for: Self-employed professionals and side hustlers

Hurdlr automates mileage, income, and expense tracking - especially great for gig workers, Uber drivers, or solo consultants.

Why it saves you time:

Auto-tracking of earnings and write-offs

Real-time tax estimates

Simple, mobile-first interface

🧠 How to Choose the Right App for You

With so many great options, how do you choose? Start by asking:

Do I need just expense tracking or full accounting?

Do I manage a team or just myself?

What tools do I already use (and need to integrate)?

Do I prefer free tools or am I ready to invest?

Don’t be afraid to try a few - most offer free trials or free tiers.

Final Thoughts: Save Time, Stay Organized, Stress Less

The best apps for business finances in 2025 aren’t just about tracking numbers - they’re about freeing up your time and mental space. With the right tools in place, your finances become less of a chore and more of a strategic advantage.

Start with the app that fits your current needs, and let your system grow as your business does. Time is money, so why not save both?

📌 Want to Know If Your Business Is Really Healthy?

At Breakspears Bookkeeping Services LLC, we help you:

✅ Track profit and cash flow side by side

✅ Get paid faster

✅ Build financial systems that support growth

👉 Explore our flat-rate bookkeeping packages

👉 Book a free discovery call to take control of your numbers - without the overwhelm.

5 Budgeting Mistakes That Are Costing You Thousands

Every dollar matters when you’re running a small business. But even the most well-meaning business owners make budgeting mistakes that quietly chip away at their profits. The good news? Once you recognize these issues, they’re easy to fix.

In this article, we’ll break down five common small business budgeting mistakes - and how you can correct them before they cost you any more money.

Every dollar matters when you’re running a small business. But even the most well-meaning business owners make budgeting mistakes that quietly chip away at their profits. The good news? Once you recognize these issues, they’re easy to fix.

In this article, we’ll break down five common small business budgeting mistakes - and how you can correct them before they cost you any more money.

💸 Mistake #1: Not Having a Budget at All

Let’s start with the obvious, many small businesses simply don’t have a formal budget. Operating without one is like driving without a map: you might move forward, but you have no idea where you're going or how much it's costing you.

Why it's costly:

Overspending on non-essential expenses

Underestimating fixed costs

Difficulty identifying financial leaks

Fix it:

Create a simple monthly or quarterly budget that includes:

Projected income

Fixed expenses (rent, payroll, subscriptions)

Variable expenses (marketing, travel, supplies)

Emergency buffer

Even a basic spreadsheet is better than flying blind.

🔍 Mistake #2: Underestimating Expenses

Optimism is great for entrepreneurs - but when it comes to budgeting, too much optimism can hurt. Many small businesses underestimate costs or forget to include irregular expenses entirely.

Commonly missed expenses:

Software renewals

Tax payments

Equipment maintenance

Annual insurance premiums

Why it’s costly:

Surprise expenses lead to cash flow issues or debt reliance.

Fix it:

Review your last 12 months of expenses and build in seasonal or annual costs. Add a 10–15% cushion for unexpected items.

⌛ Mistake #3: Ignoring Cash Flow Timing

Even profitable businesses can go under if their cash flow isn’t timed properly. A budget that shows positive income means nothing if your receivables come in after your bills are due.

Why it’s costly:

Missed payments or late fees

Reliance on credit

Stressful juggling of bills

Fix it:

Build a cash flow forecast alongside your budget:

When will cash actually come in?

When are expenses due?

Will you have enough cash on hand?

Tools like QuickBooks or Float can help automate this process.

📉 Mistake #4: Failing to Track Budget vs. Actuals

Creating a budget is just the first step: monitoring it is where the magic happens. If you’re not comparing your projected vs. actual performance, you’re missing critical insights.

Why it’s costly:

Small overages become habitual

Missed chances to correct course

No accountability

Fix it:

Do a monthly or quarterly budget review:

Where did you overspend?

Where did you save?

What trends are emerging?

Adjust future budgets accordingly.

🚫 Mistake #5: Not Budgeting for Growth

Many small business owners budget for survival, not scaling. If your budget only covers “getting by,” you’ll struggle to invest in marketing, hiring, or product development.

Why it’s costly:

Missed growth opportunities

No room to innovate

Stalled momentum

Fix it:

Add a line item for growth:

Marketing experiments

Software upgrades

Education or training

Outsourcing tasks to free up your time

Growth doesn’t happen by accident, it needs a place in your budget.

✅ Quick Recap: 5 Budgeting Mistakes to Avoid

No budget at all

Underestimating or forgetting expenses

Ignoring cash flow timing

Not reviewing actual vs. planned spending

Failing to budget for growth

Final Thoughts: Budgeting Is a Growth Tool, Not a Restriction

Budgeting isn’t about saying no - it’s about making smarter yes decisions. By avoiding these common small business budgeting mistakes, you gain clarity, control, and confidence in your financial direction.

Start small. Track progress. Adjust often. Your budget can become one of your most powerful business tools.

📌 Want to Know If Your Business Is Really Healthy?

At Breakspears Bookkeeping Services LLC, we help you:

✅ Track profit and cash flow side by side

✅ Get paid faster

✅ Build financial systems that support growth

👉 Explore our flat-rate bookkeeping packages

👉 Book a free discovery call to take control of your numbers - without the overwhelm.

The Financial Checklist Every Freelancer Needs

Freelancing gives you freedom, but with that independence comes responsibility, especially when it comes to your finances. Whether you're a graphic designer, copywriter, or developer, staying on top of your money isn’t just smart - it’s essential for long-term success.

That’s why we created the ultimate Freelancer Business Finance Checklist to help you stay organized, compliant, and in control. No accounting degree required, just a commitment to financial clarity.

Freelancing gives you freedom, but with that independence comes responsibility, especially when it comes to your finances. Whether you're a graphic designer, copywriter, or developer, staying on top of your money isn’t just smart: it’s essential for long-term success.

That’s why we created the ultimate Freelancer Business Finance Checklist to help you stay organized, compliant, and in control. No accounting degree required - just a commitment to financial clarity.

✅ 1. Open a Dedicated Business Bank Account

One of the first financial moves every freelancer should make is separating personal and business finances. Mixing the two creates confusion and can raise red flags with the IRS.

Action Steps:

Open a business checking account

Use it exclusively for freelance income and expenses

Consider getting a business credit card for larger purchases

✅ 2. Set Up a Bookkeeping System

Good bookkeeping is the backbone of any successful freelance business. Whether you use software like QuickBooks, Wave, or a spreadsheet, consistency is key.

Your system should track:

Income (clients, platforms, referrals)

Expenses (software, supplies, education, etc.)

Mileage (if you drive for business purposes)

Invoices and payment status

✅ 3. Track Every Expense

Freelancers often miss out on valuable deductions simply because they don’t track their spending. A key part of any Freelancer Business Finance Checklist is capturing every legitimate expense.

Common deductible expenses include:

Home office costs (a portion of rent, utilities)

Internet and phone

Business meals and travel

Software subscriptions

Professional development

Use apps like Expensify, Bonsai, or QuickBooks Self-Employed to automate this.

✅ 4. Create and Send Invoices Promptly

Getting paid is priority #1, so your invoicing process should be smooth and timely.